Unemployment Support

How to budget after a job loss

Making the best decisions with your finances

Links to external websites are not managed by Varo Bank, N.A. Member FDIC.

All Varo products and services mentioned below are contingent on opening a Varo Bank Account. Qualifications may apply.

Facing a job loss can be challenging and overwhelming. With bills and other monthly expenses adding up fast, we know it’s stressful to even know where to begin, especially if you have to count on unemployment benefits alone.

While the road ahead may seem uncertain, you can weather the storm with the right mindset and a little perseverance in order to make the best possible decisions with your money.

Get ready to discover some essential tips for keeping a budget while unemployed and why you have the power to make the best financial decisions through tough times.

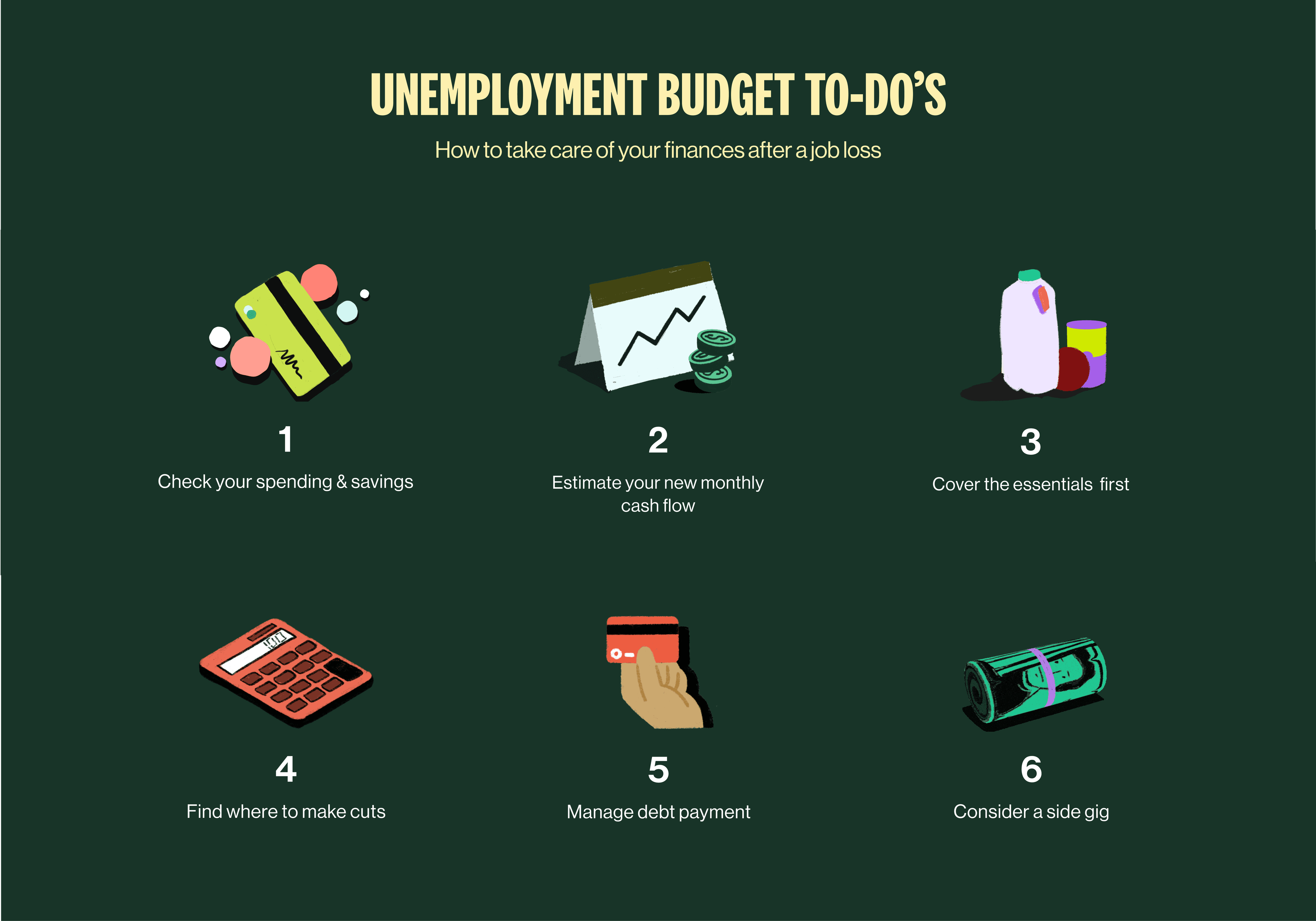

1. Check your spending and savings

We know it’s no walk in the park, but taking a hard look at your current spending habits and savings over the past few months can help you get a clearer picture of where you stand financially.

Review your bank account statements, credit card statements, and receipts to understand where your money’s been going and what you need to prioritize moving forward.

Make a list of all your anticipated monthly expenses, leaving some wiggle room for the unexpected if you can.

Check your emergency fund and estimate how long you think you’ll be able to rely on it in order to cover your expenses.

Most importantly, don’t panic—rest assured that you’re taking the right first step towards staying making the most of your money during a challenging time.

2. Estimate your new monthly cashflow

Without your usual income stream coming in, it's important to estimate your new monthly cash flow.

Find out what unemployment benefits you’re entitled to and factor these payments in.

Don’t forget to account for severance payments or other possible income sources.

Decide exactly much you can pull from your emergency fund in a pinch each month.

Realize that it may take some time before you have regular income coming in outside of unemployment benefits.

Knowing exactly what you’re working with money-wise for the time being can provide some solid clarity when it comes to covering your expenses.

3. Cover the essentials first

By understanding where you stand with cashflow, you can make sure you have the essentials covered first. You know, the important stuff.

You want your basic needs met, so prioritize food, housing, utilities, medical expenses, and transportation.

Factor in any credit card or loan payments that you’ll have to keep paying while unemployed (more on that later).

Realizing that you have the most important things covered can give you a much-needed sense of stability as you figure out your next move.

4. Find where to make cuts

This is where it can get hard. But pinpointing where you can cut back is key to staying financially healthy right now. With the basics covered, here’s a couple tips for reducing expenses while you get back on your feet.

Factor in expenses like entertainment, dining out, hobbies, or retail therapy you may need to put a pause on.

Cut out cable, TV streaming services, and other memberships or subscriptions you can live without.

You can get creative when it comes to finding ways to lower your usual expenses, like meal planning to slash grocery bills, DIY solutions to stretch resources, or fun activities that don’t cost a thing.

Take a hard look at needs over wants and be intentional with choices that protect your money.

We get it, this part isn’t fun. Remember, these cuts may be temporary—you can get back into the normal swing of things eventually.

5. Manage your debt payments

If you’re like most people, you probably have some debts that you’ll need to keep up with. Even if you’ve been a rock star with staying on top of these payments in the past, you may need to re-assess how these factor into your new budget.

Pay only the minimum payments to avoid late fees. You can start crushing your debt again when you’re back on your feet, but right now you may need to cover only the essentials.

Prioritize your high-interest debts first, as these can be the biggest drain on your cash flow as interest adds up.

Contact your creditors and explain your situation—they may offer some temporary relief or alternative repayment plans.

You may be able to get guidance from financial professionals if you need help charting the best course of action with your debt.

Again, try not to stress—this is a temporary solution to a temporary challenge.

6. Consider getting a side gig

Looking for a way to stay productive and make some extra money? This one depends on your eligibility for unemployment benefits and the rules specific to your state, as you’ll want to make sure that any side gigs don’t impact your ability to get paid the full amount you’re entitled to.

With that in mind, check out these side gig ideas for making some extra cash while you search for full time employment again.

Keeping your bills paid while unemployed is tough, but not impossible. With some careful planning and a little perseverance, you can make the best possible decisions with your money with your sights set on the next chapter and a brighter future ahead!

Find more unemployment resources

Wondering what other steps to take after a job loss? Here’s how to bounce back even stronger.

Starting a new job search? Here’s how to recover quickly from a job loss and find employment again.

Unless otherwise noted above, opinions, advice, services, or other information or content expressed or contributed by customers or non-Varo contributors do not necessarily state or reflect those of Varo Bank, N.A. Member FDIC (“Bank”). Bank is not responsible for the accuracy of any content provided by author(s) or contributor(s) other than Varo.

Showing post 15 of 112